12 February 2026

Car Finance Explained: PCP vs HP vs PCH

Difference between finance deal types

Car Finance Explained: PCP vs HP vs PCH

Buying a car is one of the biggest financial commitments most people make, and very few of us pay the full amount upfront. That's where car finance comes in. But with acronyms like PCP, HP, and PCH flying around, it can feel overwhelming. Let's break each one down in plain English so you can figure out which option suits you best.

HP — Hire Purchase

Hire Purchase is the most straightforward way to finance a car. Think of it like a traditional loan that's secured against the vehicle.

How it works: You put down a deposit (typically 10%), then pay fixed monthly instalments over an agreed term (usually 2–5 years). Once you've made every payment, the car is yours.

Key things to know:

- You don't own the car until the final payment is made, but you're building equity with every monthly payment.

- Monthly payments tend to be higher than PCP because you're paying off the entire value of the car, not just part of it.

- There's no mileage limit — drive as much as you like.

- At the end of the agreement, the car is yours outright. No balloon payments, no surprises.

- You can't sell the car during the agreement without settling the finance first.

Best suited for: People who want to own their car at the end, plan to keep it long-term, and prefer simplicity.

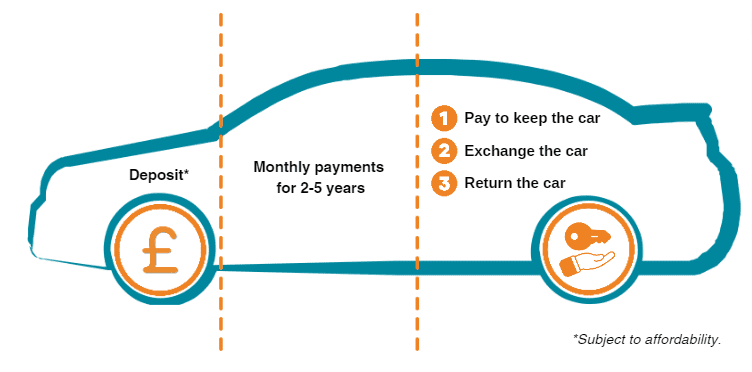

PCP — Personal Contract Purchase

PCP is the most popular form of car finance in the UK, and for good reason — it offers flexibility. However, it's a little more complex than HP.

How it works: You pay a deposit, followed by lower monthly payments over a fixed term (typically 2–4 years). The reason the payments are lower is that you're not paying off the full value of the car. Instead, a chunk of the car's value is deferred to the end of the agreement as a large final payment, known as the balloon payment (or Guaranteed Minimum Future Value — GMFV).

At the end of the agreement, you have three choices:

- Pay the balloon payment and keep the car.

- Hand the car back and walk away with nothing more to pay (as long as you've stayed within the agreed mileage and the car is in good condition).

- Use any equity as a deposit on a new PCP deal. If the car is worth more than the balloon payment, the difference is yours to put toward your next car.

Key things to know:

- Monthly payments are significantly lower than HP for the same car because you're only financing the depreciation, not the whole value.

- You'll be given an annual mileage limit (e.g. 8,000–12,000 miles per year). Go over it and you'll face excess mileage charges at the end.

- The car must be returned in good condition — fair wear and tear is fine, but dents, scratches, and interior damage could result in charges.

- You don't own the car at any point during the agreement unless you make the balloon payment.

- Many people never actually pay the balloon — they simply swap to a new car every few years.

Best suited for: People who like driving a newer car every few years, want lower monthly payments, and don't mind not owning the vehicle.

PCH — Personal Contract Hire (Leasing)

PCH is essentially a long-term rental. You're paying to use the car for an agreed period, and then you give it back. There's no option to own it at the end.

How it works: You pay an initial rental (often equivalent to 3, 6, or 9 monthly payments upfront), then fixed monthly payments for the duration of the contract (typically 2–4 years). When the contract ends, you hand the car back. That's it.

Key things to know:

- You never own the car — it always belongs to the leasing company.

- Monthly payments can be the lowest of all three options because you're purely paying for the car's depreciation during your contract.

- Maintenance packages can often be bundled in, covering servicing and tyres for a fixed monthly cost.

- Strict mileage limits apply, and excess mileage charges tend to be higher than PCP.

- The car must be returned in good condition according to the BVRLA fair wear and tear guidelines.

- Road tax is usually included in the lease.

- You have no equity in the car at any point — you can't use it as a deposit for your next deal.

- Early termination can be expensive.

Best suited for: People who want a hassle-free, predictable monthly cost and are happy to always have a car payment without ever owning the vehicle.

Side-by-Side Comparison

| Feature | HP | PCP | PCH (Lease) |

|---|---|---|---|

| Own the car at the end? | Yes — automatically | Yes — if you pay the balloon | No — never |

| Monthly payments | Highest | Medium | Lowest |

| Deposit required | Yes (typically 10%) | Yes (typically 10%) | Initial rental (3–9 months) |

| Mileage limits | No | Yes | Yes (stricter) |

| Flexibility at end | Car is yours | 3 options (keep, return, swap) | Return the car |

| Building equity? | Yes — with every payment | Only if car exceeds GMFV | No |

| Maintenance included? | No | No | Optional add-on |

| Road tax included? | No | No | Usually yes |

| Best for | Long-term ownership | Flexibility and newer cars | Low cost, hassle-free motoring |

Which One Should You Choose?

There's no single right answer — it depends on your priorities.

Choose HP if you want to own your car, plan to keep it for many years, do high mileage, or simply like the idea of eventually having no car payment at all.

Choose PCP if you enjoy driving a new car every few years, want lower monthly costs than HP, and are comfortable with mileage limits. PCP also works well if you're unsure whether you'll want to keep the car — it gives you options.

Choose PCH if you want the lowest possible monthly payment, don't care about ownership, and prefer a simple arrangement where maintenance and tax can be bundled in. Leasing is also popular with people who treat a car purely as a utility rather than an asset.

A Few Final Tips

- Always check the total amount payable, not just the monthly cost. A longer term with lower payments can end up costing significantly more overall.

- Be realistic about your mileage. Underestimating your annual mileage to get a cheaper deal on PCP or PCH will cost you at the end.

- GAP insurance is worth considering with all three options. If the car is written off or stolen, your standard insurance may not cover the full amount you owe on finance.

- Check your credit score before applying. The best rates are reserved for those with strong credit histories.

- Negotiate the price of the car, not just the monthly payment. Dealers can adjust terms to hit a monthly figure while inflating the total cost.

Need Help Buying Your Next Car?

If you're feeling overwhelmed by the options or just want expert guidance to make sure you get the best deal, we're here to help. Get in touch with us at [email protected] and let us take the stress out of your next car purchase.